Is P2P Lending Safe? The Honest Risk Rundown

Short answer: P2P lending is investing with real risk, marketed with numbers that feel like savings rates. The platforms that respect ye say this openly. Here’s the full map of what can go wrong, drawn partly from wrecks we’ve watched sink.

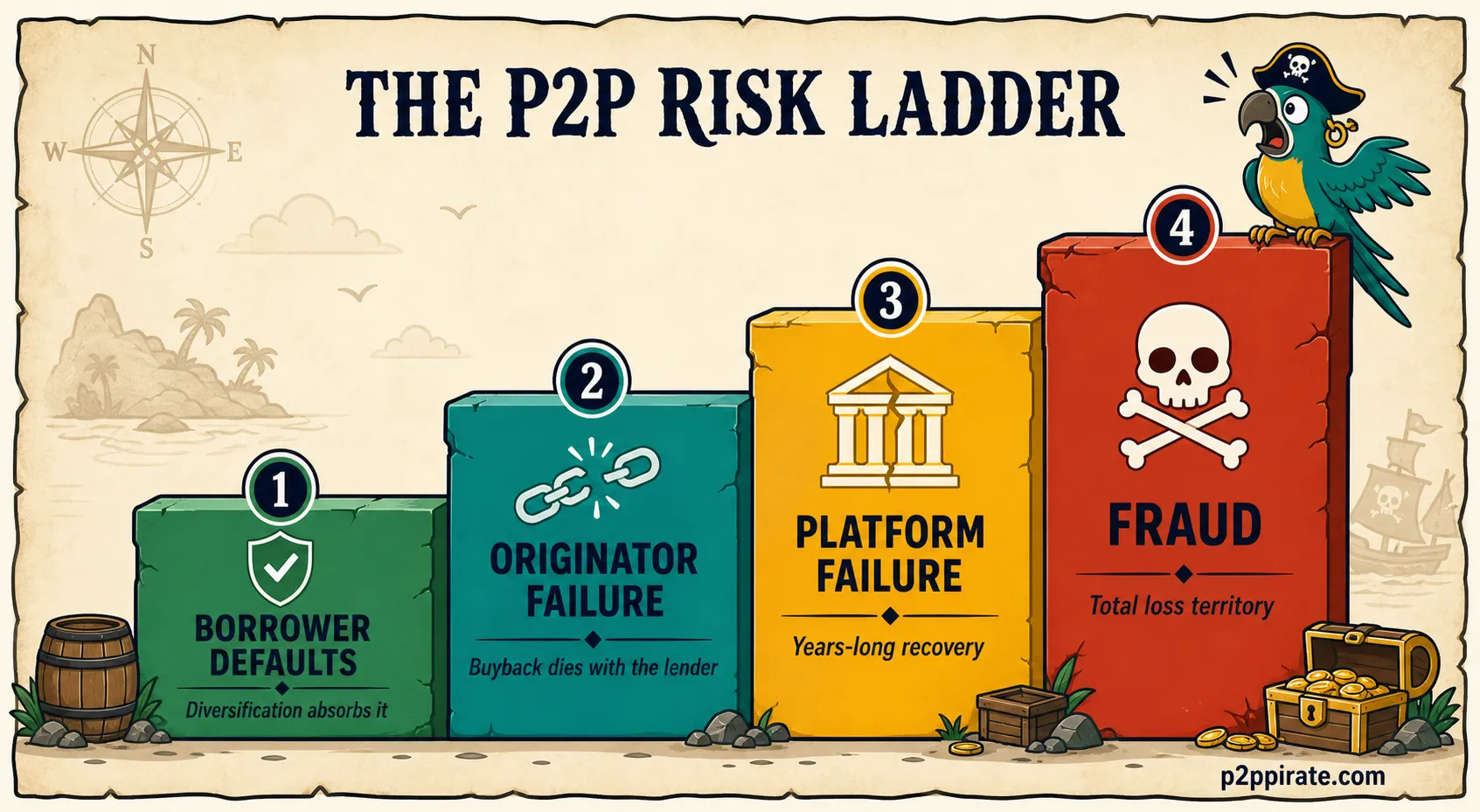

The four ways money disappears

1. Borrower defaults. The baseline risk, and ironically the most manageable one. Diversified across hundreds of loans, default rates become a statistic, not a catastrophe. Buyback guarantees mostly absorb this layer on consumer platforms.

2. Lending-company failure. The big one on marketplace platforms. When an originator collapses, its buyback obligations collapse with it, and recovery becomes a years-long legal slog. The 2020 Mintos cohort (Finko, Capital Service & co.) is the canonical case study: recoveries measured in cents on the euro, per year.

3. Platform failure or fraud. Grupeer, Envestio, Kuetzal: names every P2P investor should know before depositing anywhere. All three were outright scams or collapsed amid fraud allegations in 2019–2020, with most investor money gone. The pattern to spot: too-smooth returns, opaque originators, aggressive bonuses, no regulator. The EU’s ECSP regime and Latvia’s investment-firm licensing exist substantially because of this era.

4. Liquidity freezes. Even honest platforms can lock the exits in stress: Bondora limited Go & Grow withdrawals in March 2020; secondary markets demand discounts exactly when ye want out. Money in P2P should be money ye won’t need on a deadline.

What regulation does and doesn’t do

A license gets you: supervised custody of uninvested cash, prospectus-grade disclosure, a complaints process, and (on investment-firm platforms) ~€20,000 compensation if the broker fails. It does not underwrite your investment returns. “Regulated” narrows the disaster scenarios; it doesn’t touch the ordinary ones.

The survival rules

- Platform diversification: no platform gets more than ~20% of your P2P allocation.

- Originator diversification: inside marketplaces, spread across lending companies. They’re the real counterparties.

- Structure beats yield: prefer the 9% with a license or first-rank mortgage over the 15% with neither, unless the position is sized as a lottery ticket.

- Read the worst-year numbers, not the homepage. Recovery statistics pages tell more truth than testimonials.

- Withdraw profits sometimes. A return isn’t real until it’s been wired out at least once.

Every review on this site has a straight-faced risk box for exactly this reason. Start with the platform directory and read those boxes first.

Frequently asked questions

Can I lose money in P2P lending?

Yes. Through borrower defaults, lending-company failures, platform collapses or outright fraud (Grupeer, Envestio and Kuetzal investors lost most of their capital). Diversification limits the damage; nothing eliminates it.

Is P2P lending covered by deposit insurance?

No. P2P investments are never bank deposits. Regulated platforms offer at most an investor compensation scheme (~€20,000) that covers broker failure. It does not cover loan losses.

What percentage of my portfolio should be in P2P?

Most sensible allocations put P2P in the high-risk sleeve, commonly 5–15% of investable assets. The honest test: if every platform froze withdrawals for two years, would your plans survive?