Robocash Review 2026: One Group, One Bet, 8-10.5% on Autopilot

| Returns | 8–10.5% p.a. (advertised) |

|---|---|

| Min. investment | €10 |

| Buyback | Yes: 30-day buyback guarantee, backed by group companies. |

| Auto-invest | Yes |

| Secondary market | Yes |

| Asset classes | Consumer loans |

| Fees | None |

| Regulation | Unregulated |

| Founded | 2017 |

| HQ | HR |

3.9 / 5 · Overall

- Returns

- 4.0

- Liquidity

- 3.5

- Track record

- 4.5

- Transparency

- 4.0

- Usability

- 3.5

What we like

- ✓One-click automated portfolio from EUR 10; reinvests on its own with minimal idle cash

- ✓EUR 1.34B invested and EUR 39.9M paid out since 2017; 9.92% historical average return

- ✓30-day buyback with interest paid through the overdue period (faster than the usual 60-day trigger)

- ✓Zero fees on deposits, withdrawals, and the par-value secondary market

What we don’t

- ✕Unregulated: assignment-agreement claims, no EU licence, no investor compensation scheme

- ✕Single-group bet: platform, lenders, and buyback all sit inside UnaFinancial (2024 leverage ~25:1)

- ✕Philippine SEC revoked originator Digido's licence in May 2025 and affirmed it in February 2026

- ✕No mobile app; withdrawals under EUR 50 need manual support handling

⚓ Risk notes

Everything rests on one group: the platform, the lenders, and the buyback all sit inside UnaFinancial. The Grant Thornton-audited 2024 accounts showed debt-to-equity around 25:1 (up from ~11:1 in 2023) and net profit of just $0.6M. The Philippine SEC revoked originator Digido Finance Corp.'s licence in May 2025 and affirmed the revocation in February 2026; an appeal is pending. H1 2025 brought $5M net profit and a 37% leverage improvement, but the concentration risk is the one to re-check annually before staying invested.

Robocash is the laziest way to earn near-double-digit returns in European P2P, and that is a compliment. You create a portfolio in one click, deposit euros, and the platform buys short-term consumer loans for you. Since launching in February 2017 it has channelled EUR 1.34 billion in investments, paid investors EUR 39.9 million in interest, and delivered a 9.92% historical average return without a single investor losing money to a default.

The structure behind that record is the whole story. The platform, every loan originator on it, and the 30-day buyback guarantee all belong to one group: UnaFinancial, a Singapore-headquartered holding founded by Sergey Sedov. You are not diversifying across lenders here. You are lending to one company’s balance sheet wearing four different hats.

That balance sheet had a rough 2024: leverage spiked to roughly 25:1 and net profit fell to $0.6 million. Then the Philippine SEC revoked the licence of Digido, one of the platform’s main loan suppliers. Profits recovered sharply in 2025, but the margin of safety thinned. Robocash still earns a place in a P2P portfolio, just not a big one. This review covers exactly why.

Who’s actually behind Robocash

The legal operator is Robocash d.o.o., registered at Petračićeva 4, Zagreb, Croatia. The parent is UnaFinancial, formerly Robocash Group, with the ultimate holding company Robocash PTE. LTD. incorporated in Singapore. Founder and CEO is Sergey Sedov, with Ivan Adamovich as CFO and deputy CEO. The group runs consumer lending businesses across Asia and Europe, with its main lending operations in the Philippines and Kazakhstan.

To its credit, UnaFinancial publishes consolidated financial statements audited by Grant Thornton under IFRS, every year. Most unregulated P2P platforms do not clear that bar, so use it.

The 2024 audit is where the comfortable story cracked. Net profit came in at $0.6 million, total comprehensive result was a $6.3 million loss after currency translation, and the debt-to-equity ratio jumped from roughly 11:1 in 2023 to roughly 25:1. For a group that is simultaneously your platform, your lender, and your guarantor, 25:1 leverage is thin ice.

2025 looked better. H1 2025 net profit was $5 million on $409 million of loans issued (up 14% year on year), interest and commission income reached $106.4 million, and the group reported its liabilities-to-equity ratio improved 37% versus end-2024. By seven months in, profit hit $7 million. Recovery, yes. All-clear, not yet.

How investing on Robocash works

You do not hold loans directly. You buy claim rights to loan receivables under assignment agreements: your money goes to a UnaFinancial company, and on the due date that company returns principal plus interest. If the borrower is late, the originator must buy the claim back 30 days after the due date, with interest paid for the whole holding period including the delay.

“Enhanced protection against defaults” is the pitch. The footer of the same page states the platform holds no financial services licence. Both are true, and the gap between them is this entire review.

“Enhanced protection against defaults” is the pitch. The footer of the same page states the platform holds no financial services licence. Both are true, and the gap between them is this entire review.

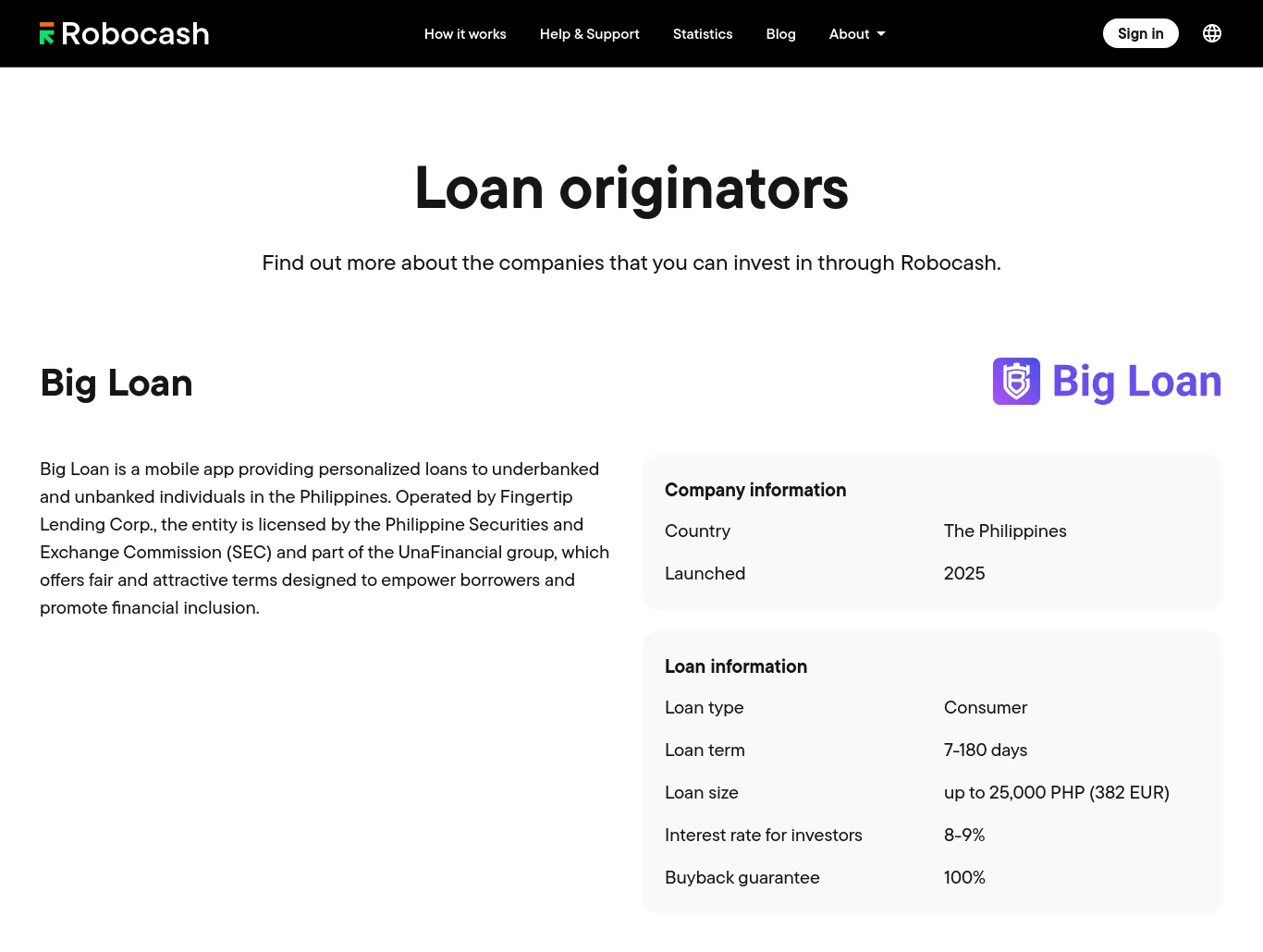

Four originator listings supply the loans, all in-group:

- Big Loan (Fingertip Lending Corp., Philippines, launched 2025): consumer loans of 7–180 days, up to 25,000 PHP (about EUR 382), paying investors 8–9%

- Digido (Digido Finance Corp., Philippines, lending since 2021, over EUR 100 million issued): pays 8–10.5%

- RC Bucharest → Kazakhstan: a Romanian special purpose vehicle channeling funding to Robocash.kz (active since 2020)

- RC Bucharest → Singapore: commercial loans of 7–1,095 days at 8–10.5%, funding the holding company itself

The day-to-day product is the automated portfolio. You set the amount and term preferences, and the system buys and reinvests for you. There is no manual loan picking worth speaking of, and that is the point: this platform is built for people who want zero involvement.

Returns: advertised vs what you’ll likely see

Current base rates run 8–10.5% depending on originator and term. The loyalty program tops that up, recalculated nightly on invested funds (not cash balance):

- Standard: EUR 50+, base rate

- Gold: EUR 20,000–49,999, +0.5%

- Platinum: EUR 50,000+, +0.8%

What you will likely see is close to the platform’s own published average: 9.92% across all investors historically. Note the direction of travel though. Older Robocash vintages paid 12%+; today’s 8–10.5% reflects both lower rates and a group that no longer needs to pay up for funding. Anyone quoting 12% is reading old reviews.

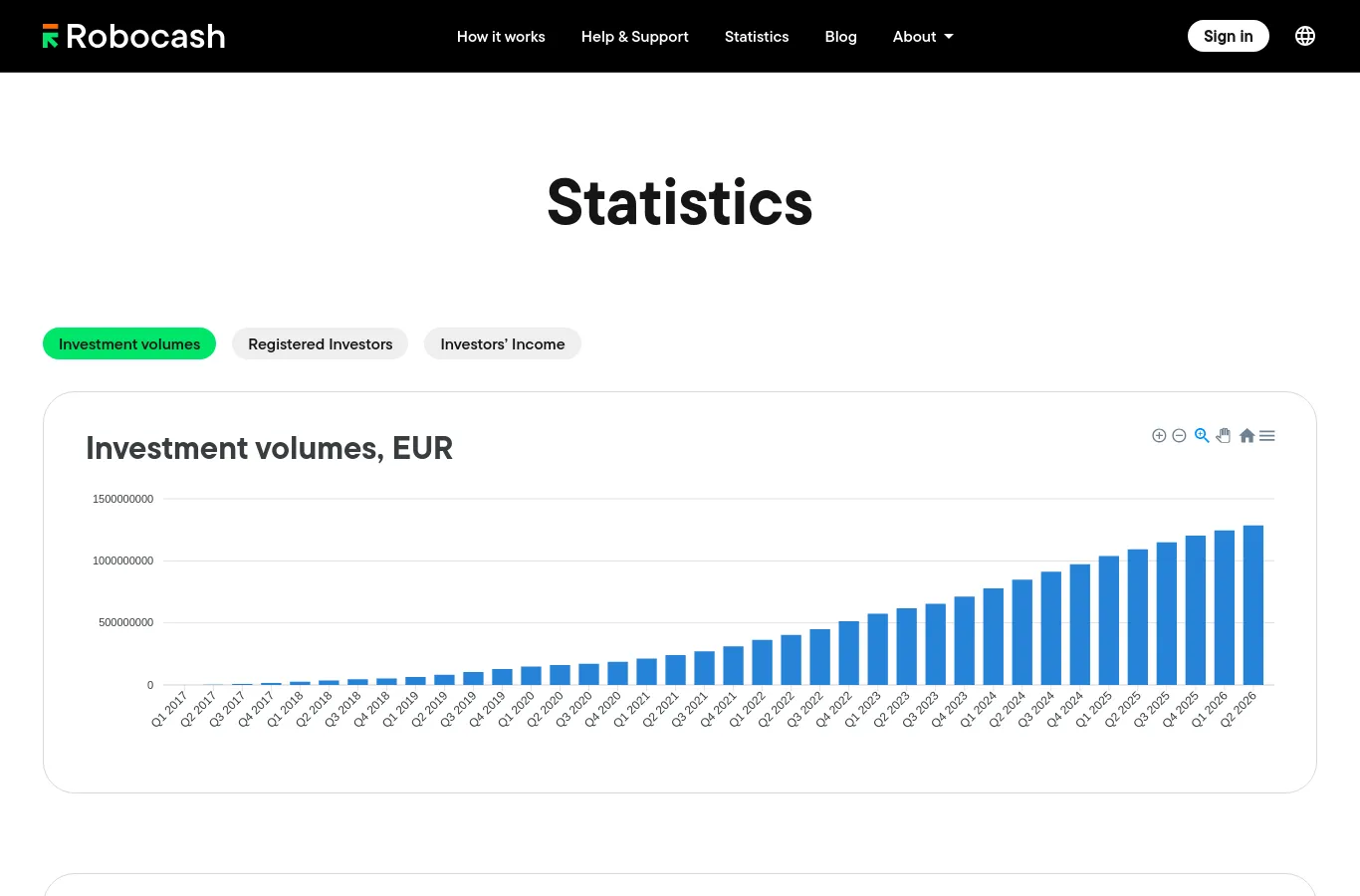

Cumulative investment volume passed EUR 1.3 billion in Q2 2026, and the curve barely flinched through the 2024 balance-sheet scare. Investor money kept flowing in while leverage peaked.

Cumulative investment volume passed EUR 1.3 billion in Q2 2026, and the curve barely flinched through the 2024 balance-sheet scare. Investor money kept flowing in while leverage peaked.

Two things eat returns here, and neither is defaults. First, cash drag: loan supply depends entirely on how much funding the group wants, so idle periods happen when UnaFinancial’s appetite drops. Second, rate compression: when the group can fund itself cheaper elsewhere, investor rates fall, and you have no competing originators to rotate into. Defaults, by contrast, have never reached investors: the 30-day buyback has been honoured since 2017, and the buyback pays your interest through the overdue period rather than skipping it.

Fees, in actual numbers

Zero. Deposits: free. Withdrawals: free. Secondary market: free, for both buyer and seller. Portfolio management: free. There is no fee schedule to audit because there is none.

The platform monetizes the spread instead. Borrowers in the Philippines and Kazakhstan pay short-term consumer rates that dwarf your 8–10.5%; the group keeps the difference, and the platform is simply its retail funding channel. That is why fees are zero: you are not the customer, you are the lender.

One operational catch worth knowing: withdrawals below EUR 50 are not processed automatically. The sum sits pending until your balance reaches EUR 50, or you email support for a manual payout. Bank transfers take up to 3 working days.

The risk that matters here

Single-group concentration, full stop. The platform that holds your account, the lenders that owe you money, and the guarantee that backstops late loans are all UnaFinancial. If the group fails, all three fail at once, and there is no regulator, no segregated custody requirement, and no investor compensation scheme standing between you and the insolvency queue. Grupeer’s 2020 collapse showed what that queue looks like for unregulated platforms: years of litigation, cents on the euro.

The 2024 accounts made this concrete. Debt-to-equity of roughly 25:1 means a small write-down in the loan book wipes a large share of equity. Net profit of $0.6 million on a group lending hundreds of millions is rounding-error profitability. The 2025 recovery ($5 million H1 net profit, leverage ratio improved 37%) is real and welcome, but one good half does not rebuild an equity cushion.

The Philippine regulatory situation compounds it. The SEC revoked Digido Finance Corp.’s financing licence and corporate registration in an order dated 9 May 2025, over four branch offices in Cavite opened without a Certificate of Authority. Digido called them marketing booths and sought reconsideration; on 18 February 2026 the SEC affirmed the revocation and directed the lender to cease operations permanently. A further appeal is pending. Meanwhile Digido loans remain available on Robocash, and the group’s newer Philippine entity, Fingertip Lending Corp. (Big Loan), holds its own SEC licence.

Every originator on the platform belongs to UnaFinancial. Two of the four listings lend in the Philippines, where the SEC revoked Digido’s licence in May 2025.

Every originator on the platform belongs to UnaFinancial. Two of the four listings lend in the Philippines, where the SEC revoked Digido’s licence in May 2025.

Read that combination plainly: a group at elevated leverage is fighting its main regulator in one of its two core markets. The buyback covers individual late loans; it cannot cover a scenario where the group itself is impaired. That scenario, not borrower defaults, is what your 8–10.5% is paying you for.

Using it day to day

Signup takes about five minutes plus standard KYC. You need to be 18+, resident in the EU, UK, or Switzerland, with a bank account in the same region. Everything runs in euros; deposits arrive by bank transfer.

After funding, the honest answer is that there is no day to day. The automated portfolio reinvests on its own, idle cash stays low when loan supply is healthy, and the account needs checking roughly never. The interface is functional but dated, more spreadsheet than fintech app, and there is no mobile app. Statements and tax reports export cleanly enough for an EU tax return.

Exits work two ways:

- Run-off: most consumer loans here are 7–183 days, so doing nothing empties the portfolio within months

- Secondary market: sell at par, zero fees, no discounts or premiums allowed

Withdrawals land in up to 3 working days, with the EUR 50 minimum quirk noted above. Support runs Monday to Friday, 9:00–17:00 CET, by email and a Zagreb phone line; response quality is decent by P2P standards.

Verdict

Robocash does one thing exceptionally well: genuinely passive 8–10.5% returns with zero fees, a 30-day buyback that has never failed, and nine years of every investor being repaid on time. The automation is the best in its class, and the group’s audited reporting beats most unregulated rivals.

The price is a concentrated bet on UnaFinancial’s solvency, taken at a moment when the group is one year past 25:1 leverage and still fighting a licence revocation in the Philippines. That is not a reason to avoid the platform. It is a reason to cap it.

Who it fits: investors who want hands-off yield, already hold diversified P2P positions elsewhere, and will actually skim one audited annual report each spring.

Who should sail elsewhere: anyone who needs a regulator between them and their money, and anyone tempted to make this a core holding.

Position sizing: keep Robocash at 5–10% of your P2P allocation, nothing more. If the 2025 full-year audit shows leverage heading back toward 2023 levels, hold. If leverage stays above 20:1 or the Philippine business deteriorates further, run off your short loans and redeploy. The loans are 7–183 days; the exit is built in.

Sources

- UnaFinancial audited financial statements for 2024 (announcement)

- UnaFinancial H1 2025 results: $5M net profit

- Robocash platform statistics

- Robocash loan originators

- Rappler: SEC revokes licence, registration of online lending firm Digido (May 2025)

- The Manila Times: Revocation of Digido licence affirmed by SEC (March 2026)

Ready to board Robocash?

Visit platformFrequently asked questions

Is Robocash safe?

Safe is the wrong frame. Robocash has repaid every investor on time since 2017 and the group publishes Grant Thornton-audited accounts, but the platform is unregulated and the platform, the lenders, and the buyback all sit inside one group, UnaFinancial. Its 2024 leverage hit roughly 25:1 before improving in 2025. Treat it as a single-counterparty bet and size it accordingly.

Is Robocash regulated?

No. The operator, Robocash d.o.o. in Zagreb, Croatia, holds no financial services licence. You buy claim rights to loan receivables under assignment agreements, not regulated securities, and no investor compensation scheme applies if anything goes wrong.

What returns does Robocash pay?

Current rates run 8% to 10.5% depending on the originator and loan term. The loyalty program adds 0.5% on portfolios above EUR 20,000 and 0.8% above EUR 50,000. The platform-wide historical average is 9.92%.

What is the minimum investment on Robocash?

EUR 10 per investment. Investing at least EUR 50 puts you in the loyalty program's Standard tier. One quirk on the way out: withdrawals under EUR 50 are held until your balance reaches EUR 50, or you contact support for a manual payout.

Can I sell Robocash investments early?

Yes, on the secondary market. Loans sell at par value with zero fees, and Robocash does not allow discounts or premiums. Liquidity is good in normal times, but the no-discount rule means you cannot price your way out if buyers disappear.

What happened to Digido, Robocash's Philippine lender?

The Philippine SEC revoked Digido Finance Corp.'s financing licence and corporate registration in an order dated 9 May 2025, citing four branch offices opened without approval, and affirmed the revocation on 18 February 2026. Digido has appealed again. Its loans remain on Robocash with the group buyback intact, but this is the live risk to watch.