What Is P2P Lending? How It Actually Works in Europe

P2P lending (peer-to-peer lending) is investing in loans. Ye put up the money, borrowers pay interest, the platform sits in the middle taking a cut from the borrower side. That’s the whole business model, and it’s why advertised investor returns of 7–16% can exist without anyone running a charity.

What you actually own

This is the part most beginners skip, and it’s the part that decides what happens when things go wrong:

- Regulated Notes (Mintos, TWINO, Viainvest, Nectaro…): securities supervised by a financial regulator, with prospectuses and an investor compensation scheme covering broker failure (not loan defaults).

- Loan claims (PeerBerry, Esketit, Robocash…): assignment agreements giving you a claim against the borrower, and in practice, reliance on the lending group’s guarantee. No regulator in the loop.

- Crowdfunding stakes (EstateGuru, Crowdpear, HeavyFinance…): ECSP-licensed platforms under the EU crowdfunding regulation, usually secured by mortgages or other collateral.

Where the yield comes from

The borrowers are mostly short-term consumer credit, small business loans, property bridge loans and agricultural loans: segments banks price expensively or won’t touch. High borrower rates fund your return and the defaults along the way. Anyone promising double-digit returns without defaults is selling ye a story.

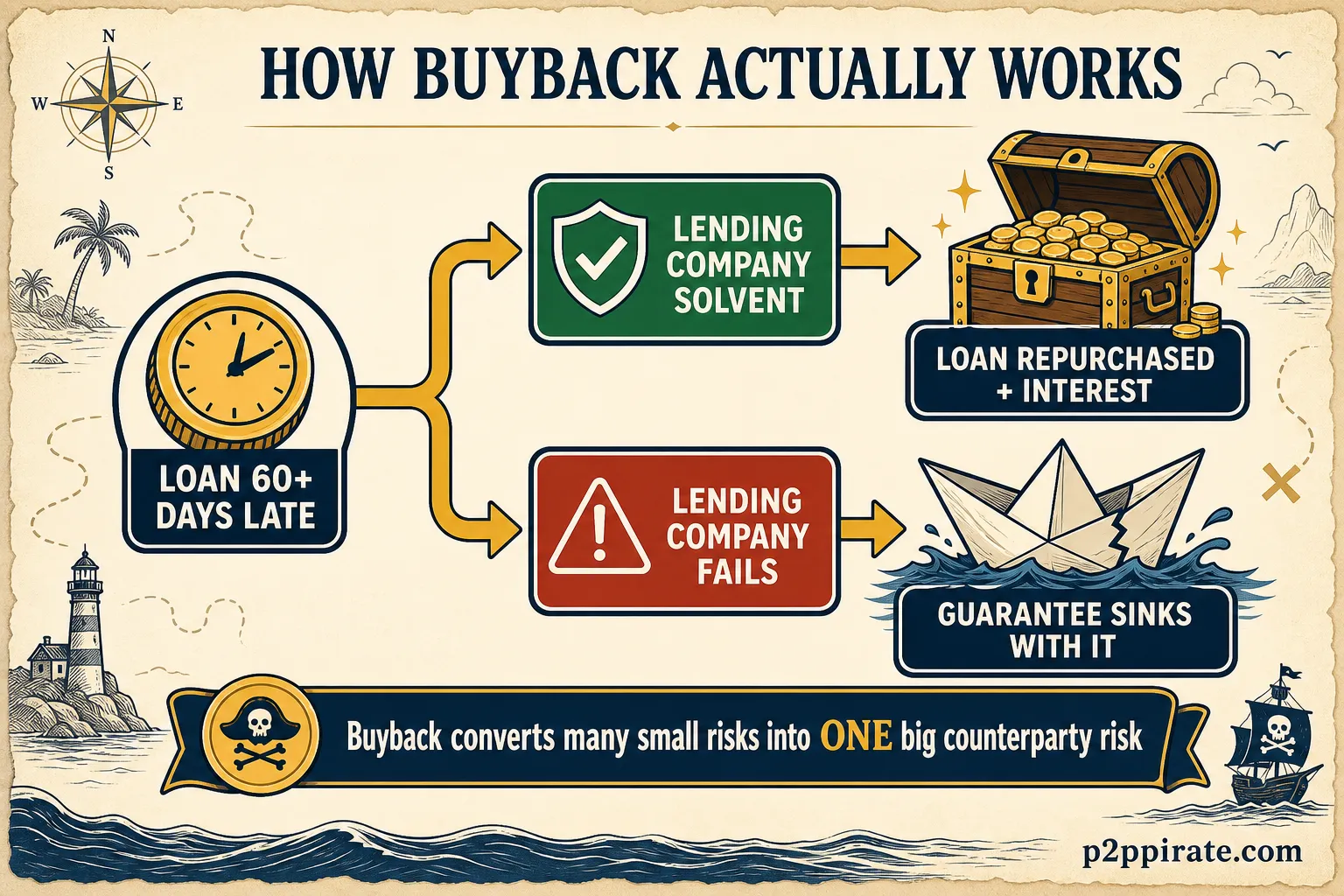

The buyback guarantee, demystified

Most consumer-loan platforms offer a buyback guarantee: if a loan goes 60+ days overdue, the lending company repurchases it with interest. It smooths your returns beautifully, right up until the lending company itself fails, at which point the guarantee fails with it. Buyback converts thousands of small borrower risks into one big counterparty risk. That’s often a good trade. It is not the absence of risk.

(Aye, we named the parrot after it.)

The five-minute due diligence

- Who regulates it? ECSP license or investment-firm license beats a promise.

- Who originates the loans? Profitable, audited group, or a mystery?

- What happened in their worst year? 2020 and 2022 separated the fleet from the driftwood.

- Can ye exit early? Secondary market, withdrawal feature, or locked until maturity?

- Does the return justify the structure? 12% unregulated is not “better” than 9% regulated. It’s differently priced risk.

Start with the best platforms ranking, read the risk guide before depositing, and check the live bonuses so your first investment at least starts with a tailwind.

Frequently asked questions

What returns can I expect from P2P lending?

European platforms advertise roughly 6–16% per year. Regulated marketplaces cluster at 7–13%, unregulated consumer-loan platforms at 10–16%. After defaults, delays and cash drag, experienced investors typically net 1–3 points below the advertised rate.

Is P2P lending the same as crowdfunding?

They overlap. P2P lending finances loans (you earn interest). Equity crowdfunding buys ownership stakes. Real-estate crowdfunding sits in between (usually property-backed loans), which is why we cover it.

How much money do I need to start?

As little as €1 (Bondora Go & Grow) or €10 (PeerBerry, Esketit). Meaningful diversification across platforms and lending companies starts making sense around €1,000.